The main aim of this article is to acquaint the reader with the concept, challenges and scope associated with rural finance. It also explores in detail the subdivision of microfinance under the head of rural finance.

According to the Census of India, 2011 the rural population is 68.84% of the total population of India. The International Fund for Agricultural Development (IFAD) defines ‘rural’ in terms of the group of houses separated by pastures, trees or farmlands with majority of the people spending time on farms. Given the large proportion of rural population, an understanding of rural finance helps in understanding the need, spending pattern and availability of financial resources for the rural poor.

The Consultative Group to Assist the Poor (CGAP) defines rural finance as 'financial services offered and used in rural areas by people of all income levels'. The various types of financial services are –

a) Deposit and Savings facility

b) Credit for Input, business or day –to-day consumption

c) Insurance for output to protect against variable demand, market price or seasonality of climate.

Based on need rural finance can be classified broadly into two sectors:

· Agriculture finance: It provides credit for agriculture-related activities like distribution, marketing, purchase of inputs and wholesaling

· Microfinance: It is provided as credit to support the rural poor.

Rural finance addresses the above mentioned needs through formal, semi-formal and informal institutions.

· Formal Channels: Nationalized Banks, Private Banks, Co-operative Banks Microfinance institutions, etc.

· Semi-formal Channels: NGOs, self-help groups, etc.

· Informal Channels: Friends, local money lenders, loan sharks etc.

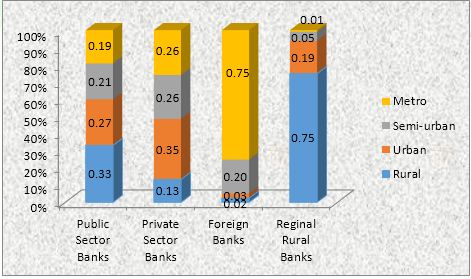

The geographic segmentation of Banks

As per, financialservices.gov.in, the average population per bank branch (APBB) as on 31.3.2013 was 12,100. For the rural population, as per the 2011 population census the number of households availing banking services was 54% of the rural population. For both type of villages, with greater than or less than a population of 2000 the number of banking outlets has increased. In these villages, the number of these banking outlets has increased from 100183 in March 2011 to 147534 in March 2012 (a 47% increase).

According to the Census of India, 2011 the rural population is 68.84% of the total population of India. The International Fund for Agricultural Development (IFAD) defines ‘rural’ in terms of the group of houses separated by pastures, trees or farmlands with majority of the people spending time on farms. Given the large proportion of rural population, an understanding of rural finance helps in understanding the need, spending pattern and availability of financial resources for the rural poor.

The Consultative Group to Assist the Poor (CGAP) defines rural finance as 'financial services offered and used in rural areas by people of all income levels'. The various types of financial services are –

a) Deposit and Savings facility

b) Credit for Input, business or day –to-day consumption

c) Insurance for output to protect against variable demand, market price or seasonality of climate.

Based on need rural finance can be classified broadly into two sectors:

· Agriculture finance: It provides credit for agriculture-related activities like distribution, marketing, purchase of inputs and wholesaling

· Microfinance: It is provided as credit to support the rural poor.

Rural finance addresses the above mentioned needs through formal, semi-formal and informal institutions.

· Formal Channels: Nationalized Banks, Private Banks, Co-operative Banks Microfinance institutions, etc.

· Semi-formal Channels: NGOs, self-help groups, etc.

· Informal Channels: Friends, local money lenders, loan sharks etc.

The geographic segmentation of Banks

As per, financialservices.gov.in, the average population per bank branch (APBB) as on 31.3.2013 was 12,100. For the rural population, as per the 2011 population census the number of households availing banking services was 54% of the rural population. For both type of villages, with greater than or less than a population of 2000 the number of banking outlets has increased. In these villages, the number of these banking outlets has increased from 100183 in March 2011 to 147534 in March 2012 (a 47% increase).

Source: financialservices.gov.in

Though India is working considerably towards financial inclusion of the poor farmers, there is a vast untapped potential given the large proportion of the rural India. Currently, many private banks are motivated to open branches in rural India because the cost of setting them is a fraction of that in a city and an efficient use of manpower can lead to profit making quite early. But still the underlying motivation is to capture the rural rich and penetrate the rural market for profit making instead of motivation for financial inclusion. However, since this target segment of rural rich is still very small, the growth rate for branches has not been as anticipated by RBI. According to RBI, the life insurance penetration forms only 4.4% of the GDP and the number of investor accounts is only 1.71% of the total population of India.

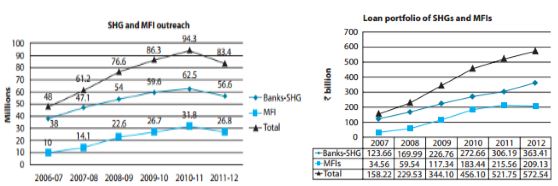

The high fiscal deficit, inflationary pressure and excessive borrowing by the government led to a cut in India’s rating. This has severely impacted the poor and people without any social security cover. The amount of microfinance credit and the SHG both decreased in their outreach though the outstanding loan amount for SHG recorded a 19% increase.

Though India is working considerably towards financial inclusion of the poor farmers, there is a vast untapped potential given the large proportion of the rural India. Currently, many private banks are motivated to open branches in rural India because the cost of setting them is a fraction of that in a city and an efficient use of manpower can lead to profit making quite early. But still the underlying motivation is to capture the rural rich and penetrate the rural market for profit making instead of motivation for financial inclusion. However, since this target segment of rural rich is still very small, the growth rate for branches has not been as anticipated by RBI. According to RBI, the life insurance penetration forms only 4.4% of the GDP and the number of investor accounts is only 1.71% of the total population of India.

The high fiscal deficit, inflationary pressure and excessive borrowing by the government led to a cut in India’s rating. This has severely impacted the poor and people without any social security cover. The amount of microfinance credit and the SHG both decreased in their outreach though the outstanding loan amount for SHG recorded a 19% increase.

Source: microfinanceindia.org

Both for SHGs and MFI, the average loan size per customer has increased to Rs 6420 and Rs 7803, respectively.

However, in the rural area, other than the credit facility, there is a need for a whole suite of products ranging from savings to insurance to pension. This need demands an ecosystem of MFIs, commercial banks, Insurance firms, SHGs and government support to address it effectively. The regulatory changes also should be able to check practises like over-selling of loans and at the same time provide enough incentive to banks and MFIs to innovate their products. Currently, many MFIs are under business pressure and have to face problems of default by clients and of arranging adequate funds. Hence the regulators, investors and other stakeholders should also extend their support in helping the MFIs and SHGs in devising the financial policies and schemes. Also, the overall objective of financial inclusion and the growth of the sector should never be lost in the whole plethora of activities.

References

Source: http://www.indicus.net/icfi/index.php/banking.html - Banking branches related news

http://articles.economictimes.indiatimes.com/2014-01-22/news/46463030_1_rural-branches-kotak-mahindra-bank-navin-puri

Financial Inclusion http://www.rbi.org.in/scripts/BS_SpeechesView.aspx?Id=862

http://financialservices.gov.in/banking/Overviewofefforts.pdf - rural finance

http://www.indianmba.com/Faculty_Column/FC553/fc553.html

http://www.microfinanceindia.org/uploads/news_attachments/20130724120608_state-of-the-sector-report-2012.pdf

http://censusindia.gov.in/2011-prov-results/paper2/data_files/india/Rural_Urban_2011.pdf

Both for SHGs and MFI, the average loan size per customer has increased to Rs 6420 and Rs 7803, respectively.

However, in the rural area, other than the credit facility, there is a need for a whole suite of products ranging from savings to insurance to pension. This need demands an ecosystem of MFIs, commercial banks, Insurance firms, SHGs and government support to address it effectively. The regulatory changes also should be able to check practises like over-selling of loans and at the same time provide enough incentive to banks and MFIs to innovate their products. Currently, many MFIs are under business pressure and have to face problems of default by clients and of arranging adequate funds. Hence the regulators, investors and other stakeholders should also extend their support in helping the MFIs and SHGs in devising the financial policies and schemes. Also, the overall objective of financial inclusion and the growth of the sector should never be lost in the whole plethora of activities.

References

Source: http://www.indicus.net/icfi/index.php/banking.html - Banking branches related news

http://articles.economictimes.indiatimes.com/2014-01-22/news/46463030_1_rural-branches-kotak-mahindra-bank-navin-puri

Financial Inclusion http://www.rbi.org.in/scripts/BS_SpeechesView.aspx?Id=862

http://financialservices.gov.in/banking/Overviewofefforts.pdf - rural finance

http://www.indianmba.com/Faculty_Column/FC553/fc553.html

http://www.microfinanceindia.org/uploads/news_attachments/20130724120608_state-of-the-sector-report-2012.pdf

http://censusindia.gov.in/2011-prov-results/paper2/data_files/india/Rural_Urban_2011.pdf

RSS Feed

RSS Feed